RBI Approves Record ₹2.87 Trillion Surplus Transfer to Government for FY26

- InduQin

- May 28

- 3 min read

Updated: May 29

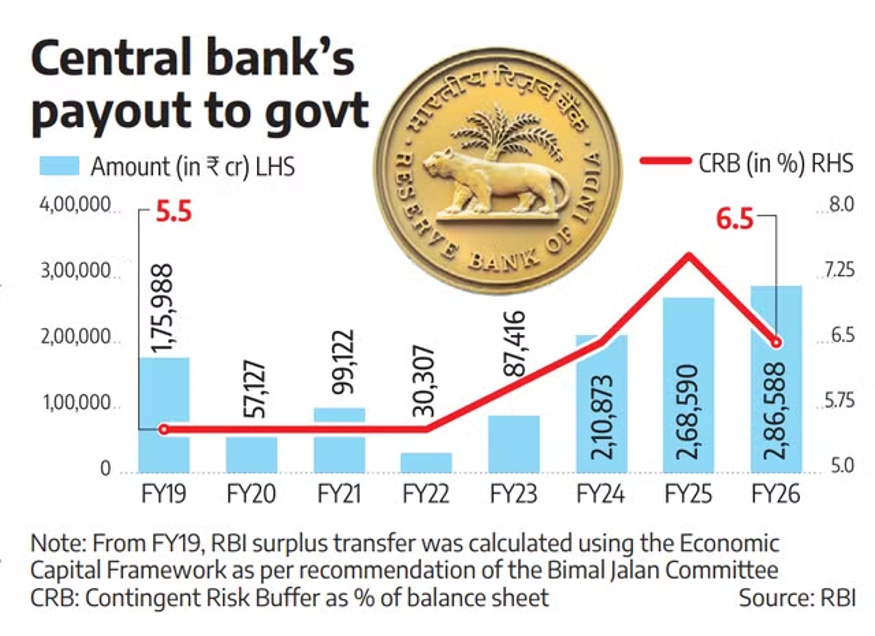

RBI approved a record ₹2.87 trillion surplus transfer to the Centre for FY26, 7% higher than FY25.

Balance sheet expanded 20.61% to ₹91.97 trillion; net income rose to ₹3.96 trillion.

CRB maintained at 6.5%; ₹1.09 trillion allocated toward risk buffer.

Higher provisioning limited surplus despite strong forex and G-sec earnings.

Transfer equals ~91% of budgeted non-tax revenue, easing fiscal pressure.

The Reserve Bank of India (RBI) has approved a surplus transfer of ₹2.87 trillion to the Central government for the financial year 2025–26 (FY26), marking the highest payout in its history. The decision, taken at the 623rd meeting of the Central Board in Mumbai under the leadership of Governor Sanjay Malhotra, reflects robust income growth and a significant expansion of the central bank’s balance sheet.

The latest transfer exceeds the previous year’s record of ₹2.69 trillion by roughly 7 per cent. The increase comes amid stronger earnings, aided in part by foreign exchange reserve sales, even as the RBI adjusted its risk provisioning framework.

Stronger Financial Performance

As of March 31, 2026, the RBI’s balance sheet had expanded by 20.61 per cent to ₹91.97 trillion. Gross income for FY26 rose 26.42 per cent compared to the prior year, while expenditure—before accounting for risk provisions—climbed 27.60 per cent.

Net income before risk provisioning and transfers to statutory reserves reached ₹3.96 trillion, up from ₹3.13 trillion in FY25. The surge in earnings provided the central bank with room to declare a higher surplus, despite elevated provisioning requirements.

Adjustment in Risk Buffer Framework

Alongside the surplus announcement, the RBI confirmed that it would maintain the Contingent Risk Buffer (CRB) at 6.5 per cent of its balance sheet for FY26. This marks a reduction from the 7.5 per cent level maintained in FY25.

Under the revised Economic Capital Framework (ECF), the permissible CRB range has been widened to 4.5–7.5 per cent, offering greater flexibility compared to the earlier 5.5–6.5 per cent band. For FY26, the central bank allocated ₹1.09 trillion toward the CRB—more than double the ₹44,861.70 crore set aside the previous year—reflecting the larger size of its balance sheet and associated risk exposures.

The RBI said its decision factored in prevailing macroeconomic conditions, its financial performance, and the need to maintain adequate buffers against potential risks.

Higher Provisioning Caps Market Expectations

Economists noted that while the surplus transfer was substantial, it fell short of some market projections. Analysts attributed this to higher-than-anticipated provisioning requirements.

With the balance sheet expanding by approximately 21 per cent year-on-year, provisioning—linked directly to asset size—rose correspondingly. Some economists also suggested that adjustments within revaluation accounts may have necessitated additional allocations to contingency reserves, though greater clarity is expected once the RBI’s annual report is published.

Despite the lower CRB ratio, the total provisioning more than doubled due to the enlarged balance sheet. Analysts pointed out that strong interest income from government securities and sizeable forex earnings—supported by about $180 billion in foreign exchange sales—helped counterbalance provisioning costs and potential mark-to-market losses.

Fiscal Implications Remain Complex

Although the record dividend provides meaningful support to government finances, economists caution that fiscal pressures persist. Rising subsidy commitments, particularly for fertilisers and fuel, along with weaker-than-expected tax collections and lower dividends from oil marketing companies, could strain the Centre’s fiscal math.

Some estimates suggest that the fiscal deficit for FY27 could overshoot the budgeted target of 4.3 per cent of GDP by around 40 basis points, assuming crude oil averages $95 per barrel during the year. Oil prices have climbed amid geopolitical tensions in West Asia, adding uncertainty to fiscal projections.

At the same time, the higher allocation to the CRB is seen as strengthening the RBI’s capacity to manage financial market volatility in response to shifting domestic and global conditions. The FY26 surplus transfer accounts for nearly 91 per cent of the government’s projected non-tax revenue, offering partial relief to the exchequer during a period of geopolitical and economic uncertainty.

Overall, the RBI’s latest surplus decision underscores both the strength of its financial position and the balancing act required to safeguard stability while supporting public finances.

Comments